How do I open an offshore bank account? This comprehensive guide dives deep into the world of offshore banking, providing a clear roadmap for navigating the complexities and understanding the crucial factors involved. We’ll explore the nuances of eligibility, jurisdictions, costs, and regulations, ensuring you’re well-informed before taking the plunge.

From understanding the fundamental differences between offshore and domestic accounts to the critical steps in the account opening process, this guide equips you with the knowledge needed to make an informed decision. We’ll also delve into tax implications, security concerns, and the vital importance of regulatory compliance, enabling you to confidently navigate this often-complicated territory.

Understanding Offshore Bank Accounts

Offshore bank accounts are financial accounts held in a country different from the account holder’s residence. These accounts often offer unique features, but they also come with specific considerations and regulations. Understanding the nuances is crucial for anyone considering opening one.Offshore bank accounts are distinct from domestic accounts in several key ways. Domestic accounts are typically regulated by the country where the bank is located, whereas offshore accounts are subject to the laws and regulations of the country where the bank is situated.

This difference in jurisdiction can lead to varying levels of transparency and accountability. This can also influence the tax implications for account holders.

Key Differences Between Offshore and Domestic Accounts

Offshore accounts often provide a different tax environment compared to domestic accounts. Tax implications can vary significantly, and it’s crucial to consult with a financial advisor to understand the specific tax implications for your situation. This is a critical factor to consider when choosing between offshore and domestic accounts. Offshore jurisdictions sometimes have lower or different tax rates, leading to potential savings.

However, this can be offset by the complexity of international tax reporting.

Types of Offshore Bank Accounts

Various types of offshore bank accounts cater to different needs. These accounts include savings, checking, and investment accounts. Savings accounts typically offer low-risk, low-return options. Checking accounts are designed for everyday transactions. Investment accounts are specifically for growing wealth.

The specific offerings will vary significantly between different offshore banks and jurisdictions.

Common Misconceptions About Offshore Accounts

There are common misconceptions about offshore bank accounts. One misconception is that they are inherently illegal or used for illicit activities. Offshore accounts are legitimate financial instruments used by individuals and businesses for various reasons. Another misconception is that they provide complete anonymity. Offshore jurisdictions have varying degrees of transparency and regulations, and complete anonymity is not guaranteed.

The actual level of privacy varies widely depending on the specific jurisdiction.

Comparison of Offshore and Domestic Bank Accounts

| Account Type | Offshore Account Fees | Domestic Account Fees | Regulations |

|---|---|---|---|

| Savings | Potentially lower minimum balance requirements, varying monthly maintenance fees. | Typically higher minimum balance requirements, often lower monthly maintenance fees. | Subject to regulations of the offshore jurisdiction. |

| Checking | Transaction fees, international wire transfer fees, account maintenance fees. | Transaction fees, ATM fees, and monthly maintenance fees. | Subject to regulations of the offshore jurisdiction. |

| Investment | Investment account management fees, investment performance-based fees. | Investment account management fees, investment performance-based fees. | Subject to regulations of the offshore jurisdiction. |

The table above provides a general comparison. Specific fees and regulations will vary significantly depending on the individual bank and the offshore jurisdiction. Consult with financial advisors to understand the particular conditions for your needs.

Eligibility Criteria: How Do I Open An Offshore Bank Account

Opening an offshore bank account isn’t as simple as just filling out a form. Strict eligibility criteria exist, often varying significantly depending on the jurisdiction. Understanding these requirements is crucial for a successful application. These regulations are in place to maintain financial stability and prevent illicit activities.Offshore banking jurisdictions, while offering potential benefits, are governed by regulations that prioritize due diligence and compliance.

This includes stringent checks to verify the applicant’s identity and financial background. A thorough understanding of these criteria is essential to avoid delays or rejections.

Requirements for Opening an Offshore Account

Eligibility criteria typically involve nationality, residency, and income. These requirements differ substantially between jurisdictions, and a prospective account holder must meticulously examine the specific regulations of the chosen jurisdiction. Meeting these requirements demonstrates a legitimate need for the account, reinforcing the financial institution’s commitment to responsible banking practices.

- Nationality: Some jurisdictions might prefer applicants holding a specific nationality, while others might not have any restrictions. For example, the Isle of Man welcomes clients from various nations, but certain jurisdictions might have stricter criteria, like a requirement for citizens of a particular country. The specific criteria are often published on the relevant authorities’ websites.

- Residency: Most jurisdictions require some form of residency, even if it’s a minimum stay or specific requirements for visa status. This requirement often depends on the type of account and the intended usage. This ensures that the offshore account is used for legitimate purposes.

- Income: A minimum income threshold is often a standard requirement. The specific amount varies considerably based on the jurisdiction and the type of account. For example, high-net-worth individuals might face different income standards compared to individuals seeking a basic account. The higher the income threshold, the more stringent the due diligence process.

Role of Due Diligence

Due diligence is a cornerstone of the offshore banking process. It involves a thorough investigation of the applicant’s identity and financial situation to ensure compliance with regulations. This process helps prevent money laundering and other financial crimes.

- Verification of Identity: This includes verifying the applicant’s passport, driver’s license, or other identification documents. The depth of verification depends on the jurisdiction and the account type. This level of scrutiny helps to prevent fraudulent activities and ensure the account is legitimately held.

- Scrutiny of Financial Background: This involves examining the applicant’s financial records to ensure their income aligns with the account application. The specific requirements for documentation vary greatly between jurisdictions. This is critical for establishing the legitimacy of the applicant’s need for the account.

Reasons for Account Application Rejection

Account applications can be rejected for various reasons. Common causes include insufficient documentation, failure to meet the required income threshold, or discrepancies in the provided information. Furthermore, if the applicant is deemed a high-risk individual, the application might be rejected.

- Insufficient Documentation: Providing incomplete or inaccurate documentation can lead to rejection. This includes missing or incorrect information on the required forms.

- Non-compliance with Income Thresholds: If the applicant’s income does not meet the minimum requirement, the application might be rejected.

- Discrepancies in Information: Inconsistent information provided in the application or supporting documents can result in rejection. This emphasizes the importance of meticulous accuracy.

Implications of Not Meeting Eligibility Criteria

Failing to meet the eligibility criteria can lead to account application rejection, delays, or even legal ramifications. It’s essential to thoroughly research and understand the specific requirements before applying. Understanding the implications can help prospective account holders prepare adequately.

Typical Eligibility Requirements by Jurisdiction

| Jurisdiction | Nationality | Residency | Income |

|---|---|---|---|

| Cayman Islands | No restrictions | Minimum stay or visa | High |

| British Virgin Islands | No restrictions | Minimum stay or visa | High |

| Isle of Man | No restrictions | Minimum stay or visa | Moderate |

Offshore Banking Jurisdictions

Opening a bank account offshore can offer compelling advantages, but the choice of jurisdiction significantly impacts the experience. Navigating the complexities of various offshore banking centers requires a deep understanding of their specific regulations and potential pitfalls. This section delves into popular jurisdictions, examining their advantages, disadvantages, and regulatory landscapes.Understanding the nuances of different offshore banking jurisdictions is crucial for making informed decisions.

Factors like tax benefits, privacy protections, and political stability vary greatly between countries, affecting the long-term viability and security of your offshore account. A thorough comparison is vital to selecting a jurisdiction that aligns with your financial goals and risk tolerance.

Popular Offshore Banking Jurisdictions

Choosing the right offshore banking jurisdiction is critical for successful financial planning. Each jurisdiction has its own unique set of advantages and disadvantages, impacting factors such as tax implications, regulatory oversight, and potential risks. A comparative analysis of these factors is essential.

- Cayman Islands: Known for its robust financial services sector and low tax environment, the Cayman Islands attract numerous international businesses and high-net-worth individuals. Its stable political climate and strong regulatory framework contribute to its appeal. However, strict compliance regulations are in place, and navigating these requirements can be challenging for some.

- British Virgin Islands (BVI): The BVI enjoys a reputation for its excellent privacy protections and favorable tax regime, making it a popular choice for offshore banking. Its established legal framework and strong financial infrastructure create a secure environment for financial transactions. However, the BVI’s reliance on international partnerships can influence its long-term stability.

- Panama: Panama offers a relatively low tax environment and a long history of financial services. Its strategic location and established banking infrastructure attract international clients. However, concerns regarding political stability and regulatory scrutiny have emerged, creating potential risks.

- Switzerland: While not solely an offshore jurisdiction, Switzerland’s reputation for banking secrecy and neutrality has made it a significant player in international finance. Its highly regulated financial system provides a high degree of security and discretion. However, Swiss banking regulations are complex and navigating them can be challenging.

- Luxembourg: Luxembourg has emerged as a significant center for European financial services. Its robust regulatory framework, low tax rates, and strategic location offer compelling advantages. However, the jurisdiction’s regulatory environment may be less favorable to certain types of transactions compared to other options.

Advantages and Disadvantages of Each Jurisdiction

Each jurisdiction presents a unique combination of advantages and disadvantages for offshore banking. Understanding these factors is critical for making an informed decision. A thorough analysis of these aspects is vital.

- Tax Benefits: Tax benefits are a primary driver for many offshore banking accounts. Jurisdictions offering low or no taxation on certain financial activities can significantly reduce the tax burden for individuals and corporations. However, the specific tax benefits often depend on individual circumstances and the nature of financial activities.

- Privacy and Confidentiality: Privacy and confidentiality are essential concerns for many offshore banking clients. Some jurisdictions offer stringent privacy protections, safeguarding client information and transactions. However, these protections are not absolute and can be influenced by international legal obligations.

- Political Stability: Political stability is a crucial factor in assessing the long-term viability of an offshore banking account. A stable political environment reduces the risk of unforeseen changes in regulations or policies that could impact financial activities. Assessing political risk is critical to minimizing potential financial losses.

Regulatory Environments Comparison

Comparing regulatory environments across various offshore banking jurisdictions is essential for assessing the risks and rewards associated with each option. The regulatory frameworks significantly influence the safety and security of your offshore investments.

| Jurisdiction | Tax Benefits | Privacy | Political Stability |

|---|---|---|---|

| Cayman Islands | Low | Strong | High |

| BVI | Low | Strong | High |

| Panama | Low | Moderate | Moderate |

| Switzerland | Moderate | Strong | High |

| Luxembourg | Low | Strong | High |

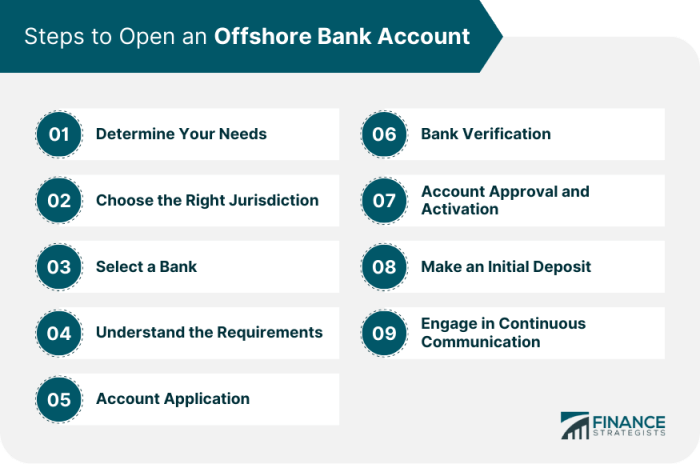

Account Opening Process

Opening an offshore bank account is a multi-step process requiring careful planning and meticulous attention to detail. Success hinges on understanding the specific procedures of each jurisdiction and adhering to the bank’s regulations. This section details the steps involved, required documentation, expected timelines, and potential obstacles.

Account Opening Steps

The process of opening an offshore bank account is not standardized across all jurisdictions. Each bank and jurisdiction has its own specific procedures. Generally, the process involves several key steps.

- Initial Inquiry and Application: Begin by contacting the bank directly to initiate the application process. Request information about their offshore banking services and the account type that best suits your needs. Complete the application form meticulously, providing accurate and complete information. This initial step is crucial for establishing a foundation for the subsequent stages. The application form often includes questions about your identity, financial history, and intended use of the account.

- Verification and Due Diligence: The bank will verify your identity and background through a due diligence process. This process typically involves reviewing supporting documentation, such as passports, driver’s licenses, and utility bills, to confirm your identity and address. The level of scrutiny varies depending on the jurisdiction and the bank’s risk assessment criteria. The goal is to ensure compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations.

- Document Submission and Review: Submit the required documentation promptly and accurately. The required documentation varies significantly by jurisdiction and bank. Common documents include passports, proof of address, and proof of income. The bank will thoroughly review the submitted documents to verify their authenticity and ensure compliance with regulatory requirements. Ensure all documents are current and correctly formatted.

- Account Setup and Activation: Once the bank approves your application and verifies your documentation, they will set up your account. This process includes assigning an account number, opening the account, and establishing any necessary security measures. This stage can take a few business days to several weeks depending on the bank and the specific circumstances.

- Funding and Access: After account activation, you can fund the account using various methods such as wire transfers. The bank will provide instructions on how to proceed. You will receive login credentials to access your account online and manage your funds. This step completes the account opening process.

Documentation Requirements

Thorough preparation of documentation is essential for a smooth account opening process. The specific documentation required varies depending on the offshore jurisdiction and the bank. However, some commonly required documents include:

- Passport: A valid passport is generally required to verify your identity.

- Proof of Address: Utility bills, bank statements, or lease agreements are common forms of proof of address.

- Proof of Income: Bank statements, pay stubs, or tax returns are examples of proof of income documents. The specific requirements will vary according to the bank and its assessment of risk.

- Identification Documents: Depending on the jurisdiction and bank, other documents such as driver’s licenses, birth certificates, or national ID cards might be required.

Typical Timeframe

The time required to open an offshore bank account varies significantly depending on factors like the complexity of the application, the bank’s workload, and the jurisdiction’s regulatory requirements. It’s crucial to understand that there is no fixed timeframe for account opening. Expect the process to take several weeks, if not months. Communicate with the bank to inquire about their typical processing times.

Potential Delays and Solutions

Delays in account opening can occur due to various reasons, including incomplete or inaccurate documentation, discrepancies in information, or regulatory compliance checks. If delays occur, proactively contact the bank to understand the reason and explore solutions. Address any issues promptly to minimize delays. Providing additional information or clarifying discrepancies will expedite the process.

Costs and Fees

Source: weebly.com

Opening an offshore bank account isn’t free. Understanding the various costs and fees is crucial for making an informed decision. Hidden fees can significantly impact your bottom line, so meticulous research is key. Offshore banking jurisdictions often vary in their fee structures, adding another layer of complexity. This section will detail typical fees, compare them across different jurisdictions, and highlight the importance of careful cost analysis before committing.

Typical Fees Associated with Offshore Bank Accounts

Offshore bank accounts, like any financial product, come with associated costs. These can include account maintenance fees, transaction fees (for wire transfers, debit card usage, etc.), and potentially, minimum balance requirements. These fees can fluctuate significantly depending on the chosen jurisdiction and the specific bank. A crucial aspect is understanding the fee structure upfront.

Figuring out how to open an offshore bank account can be tricky. Understanding the nuances of off sure account structures and regulations is crucial. However, thorough research into the specific requirements of the jurisdictions you’re considering is essential to navigating the process successfully.

Comparison of Fees Across Different Offshore Jurisdictions

Fees for offshore banking vary considerably between jurisdictions. Some jurisdictions may emphasize low or no account maintenance fees, but might charge higher transaction fees. Others may have higher account maintenance fees but lower transaction costs. A comparative analysis of fees is essential. Comparing fees across different jurisdictions is vital to finding the most cost-effective solution.

Hidden Costs and How to Avoid Them

Hidden costs in offshore banking are common. These might include foreign exchange fees, conversion charges, or unexpected charges for specific services. Researching the terms and conditions thoroughly is vital. Thoroughly reviewing the terms and conditions before signing up is the best way to avoid hidden fees. Always ask about all fees associated with account usage, such as international wire transfers, before opening the account.

Importance of Understanding All Fees Before Opening an Account

Knowing the total cost of an offshore account is essential for financial planning. Ignoring fees can lead to unexpected expenses, potentially negating the benefits of offshore banking. Before making a decision, understanding the full cost structure, including all potential fees and charges, is essential.

Table: Breakdown of Typical Account Opening and Maintenance Fees

| Offshore Banking Center | Account Opening Fee (USD) | Monthly Maintenance Fee (USD) | Transaction Fee per Wire Transfer (USD) | Minimum Balance Requirement (USD) |

|---|---|---|---|---|

| Cayman Islands | 500-1500 | 100-250 | 50-100 | 10,000-50,000 |

| British Virgin Islands | 300-1000 | 50-200 | 25-75 | 5,000-25,000 |

| Switzerland | 1000-5000 | 250-750 | 100-200 | 25,000-100,000 |

| Hong Kong | 200-800 | 50-150 | 25-50 | 10,000-50,000 |

Note: Fees are estimates and can vary significantly based on the specific bank and account type. Always verify with the bank directly.

Tax Implications of Offshore Bank Accounts

Source: financestrategists.com

Offshore bank accounts, while offering potential benefits, come with complex tax implications. Understanding these implications is crucial before considering opening such an account. Navigating the tax landscape surrounding offshore accounts requires careful consideration and, ideally, professional guidance. Failure to comply with tax regulations can lead to significant penalties and legal repercussions.

Tax Optimization Strategies

Tax optimization, when conducted legally, involves structuring financial affairs to minimize tax liabilities within the bounds of applicable laws. Offshore accounts can be used strategically to achieve this goal, particularly when combined with other legitimate financial planning tools. For example, certain jurisdictions offer favorable tax treaties or lower tax rates on specific income streams, potentially leading to substantial savings for eligible individuals.

It’s essential to remember that the legality and appropriateness of such strategies depend on individual circumstances and local regulations.

Potential Tax Consequences of Non-Compliance

Non-compliance with tax laws related to offshore accounts can lead to severe consequences. These penalties can include substantial fines, interest charges, and even criminal prosecution. Failure to report offshore assets can result in significant penalties, and in some cases, lead to the seizure of assets. The potential consequences of non-compliance highlight the importance of consulting with a qualified tax professional.

Importance of Consulting a Tax Professional

A qualified tax professional can assess your specific circumstances and advise on appropriate strategies for minimizing tax liabilities while ensuring full compliance with all applicable laws. They can guide you through the complexities of offshore account management and help you understand the potential tax implications. This expert guidance is invaluable for navigating the intricacies of international tax regulations.

Seeking professional advice is paramount to avoid potential legal issues.

Key Tax Considerations for Opening Offshore Accounts

- Jurisdictional Tax Laws: Thoroughly research the tax laws of the jurisdiction where you intend to open the offshore account, and the laws of your home country. This is crucial for determining the tax implications and ensuring compliance with both jurisdictions. Differences in tax treaties and regulations can significantly impact the overall tax burden.

- Reporting Requirements: Familiarize yourself with the reporting requirements in your home country. Understanding and adhering to these requirements is essential for avoiding penalties and maintaining compliance. Some jurisdictions require the reporting of offshore assets, which must be accurately and promptly reported.

- Income Sources: Analyze your income sources and how they might be impacted by the offshore account. Different income types (e.g., investment income, business profits) might be subject to different tax rates and reporting obligations in different jurisdictions. Proper categorization and reporting of income sources is vital.

- Tax Treaties: Review any tax treaties between your home country and the offshore jurisdiction. Such treaties might offer specific exemptions or reduce tax liabilities. The terms of these agreements can significantly affect the overall tax impact.

- Asset Valuation: Understand the valuation methods for your assets held in the offshore account. Accurate valuation is crucial for proper reporting and tax calculations. Asset valuation methodologies vary across jurisdictions.

Security and Privacy

Opening an offshore bank account often raises concerns about security and privacy. Understanding the measures taken by offshore banks and the regulations governing these accounts is crucial for making informed decisions. Offshore jurisdictions often boast strict confidentiality, but the landscape varies significantly. This section dives deep into the security measures and privacy regulations surrounding offshore banking, helping you navigate these complexities.Offshore banks employ robust security measures to protect client data.

These measures go beyond standard banking practices, often incorporating advanced technologies and procedures to prevent fraud and unauthorized access. Privacy regulations in offshore jurisdictions are designed to maintain client confidentiality, but these regulations also differ significantly between jurisdictions. It’s important to assess these differences and select a jurisdiction and bank that aligns with your specific needs and risk tolerance.

Opening an offshore bank account involves navigating complex regulations and finding a reputable financial institution. Understanding the intricacies of the process, including due diligence and compliance, is crucial. Crucially, you also need to consider how much money is in offshore accounts globally, which can vary greatly depending on factors like account type and jurisdiction. how much money is in offshore accounts This information will help you make informed decisions about your financial strategy and tailor your approach to opening an offshore account effectively.

Security Measures Employed by Offshore Banks, How do i open an offshore bank account

Offshore banks implement a range of security measures to protect client funds and data. These measures include robust authentication protocols, advanced encryption techniques, and rigorous internal audits. The specific measures vary depending on the bank and the jurisdiction, but generally include:

- Multi-factor authentication: Requiring multiple forms of identification, like passwords, security tokens, or biometric scans, to access accounts.

- Advanced encryption: Using sophisticated encryption methods to protect sensitive data transmitted between clients and the bank.

- Regular security audits: Conducting thorough audits to identify and address any potential security vulnerabilities.

- 24/7 monitoring: Employing systems to continuously monitor account activity for suspicious transactions.

Privacy Regulations in Offshore Jurisdictions

Offshore jurisdictions vary significantly in their privacy regulations. Some jurisdictions offer strong protections for client confidentiality, while others may have less stringent rules. The level of protection afforded to clients is often tied to the jurisdiction’s reputation for maintaining secrecy. This is a critical factor in choosing a suitable offshore bank.

- Data protection laws: Different jurisdictions have varying data protection laws and regulations, impacting the privacy and security of client information.

- Tax information exchange agreements (TIEAs): Offshore jurisdictions may have signed TIEAs with other countries, potentially impacting the confidentiality of client financial information.

- Transparency requirements: Some jurisdictions have requirements for transparency in offshore financial accounts, potentially exposing some client information.

Comparison of Privacy Standards

Comparing the privacy standards of different offshore banking centers is essential. A thorough comparison should consider factors such as the jurisdiction’s track record on protecting client confidentiality, the strength of its data protection laws, and any relevant tax information exchange agreements. Consider the potential impact of these factors on your specific financial needs and circumstances.

| Offshore Banking Center | Privacy Regulations | Security Measures |

|---|---|---|

| Cayman Islands | Strong confidentiality protections; stringent data protection laws. | Advanced encryption, multi-factor authentication, and rigorous internal controls. |

| British Virgin Islands | Strong reputation for confidentiality; well-established legal framework. | Advanced security measures to protect sensitive data; frequent security audits. |

| Switzerland | Historically strong confidentiality; strict banking secrecy laws. | Advanced security measures and strict internal controls. |

Choosing a Reputable and Secure Offshore Bank

Selecting a reputable and secure offshore bank is paramount. Thorough research, due diligence, and understanding of the jurisdiction’s legal framework are critical. Look for banks with a long history of stability and a strong commitment to security. Referrals and reviews from reputable sources can provide additional insight. A thorough understanding of the risks and benefits is vital to making the right decision.

Regulatory Compliance

Source: isog.org

Opening an offshore bank account isn’t just about avoiding taxes; it’s about navigating a complex web of regulations. Understanding the regulatory landscape is crucial for ensuring compliance and avoiding potential legal issues. Compliance isn’t optional; it’s a necessity for maintaining a legitimate and secure financial setup.

The Offshore Banking Regulatory Landscape

The global regulatory environment surrounding offshore banking is intricate and constantly evolving. Different jurisdictions have varying regulations, and these regulations often intersect with international standards. This necessitates a thorough understanding of the specific rules and guidelines governing offshore banking in the chosen jurisdiction. Failure to adhere to these regulations can lead to severe penalties and reputational damage.

Figuring out how to open an offshore bank account involves more than just a few clicks. Understanding the nuances of different offshore banking options is crucial, and comparing various providers is key. For a detailed look at offshore bank account comparison, check out this resource: offshore bank account comparison. Once you’ve got a grasp on the options, you can start making informed decisions about the best account for your needs.

Importance of International Regulations

Adherence to international regulations is paramount for offshore accounts. International standards, such as those set by the Financial Action Task Force (FATF), aim to combat money laundering and terrorist financing. Offshore jurisdictions often adopt and adapt these standards to maintain their financial integrity and reputation. Compliance with these regulations fosters trust and stability in the global financial system.

Figuring out how to open an offshore bank account often starts with understanding what offshore banking actually entails. Offshore banking, essentially, involves banking outside of your home country. To get the ball rolling on opening an account, researching reputable financial institutions specializing in international banking is crucial. What is offshore banking and the specific requirements for each institution will vary greatly, so thorough research is essential.

This understanding is vital to opening a successful offshore account.

Potential Risks of Non-Compliance

Non-compliance with regulatory requirements can have significant repercussions. These can include hefty fines, legal action, and the closure of the account. Furthermore, non-compliance can damage the reputation of both the account holder and the financial institution. Such consequences can severely impact financial stability and personal assets. Consider a case where a business failed to comply with AML regulations, leading to substantial penalties and reputational damage.

Know Your Customer (KYC) Procedures

KYC procedures are critical in offshore banking. They are designed to verify the identity of account holders and assess their risk profile. These procedures typically involve documentation requests and due diligence checks. Failure to comply with KYC regulations can lead to the account being flagged and potentially closed. This is essential to prevent the account from being used for illicit activities.

Anti-Money Laundering (AML) Regulations

AML regulations are crucial for preventing money laundering and terrorist financing. These regulations vary across jurisdictions but generally involve similar principles. These principles typically include customer identification, transaction monitoring, and reporting suspicious activities. Consider a scenario where a bank failed to report suspicious transactions, leading to a substantial fine and legal action.

- Common Offshore Jurisdictions and their AML Regulations: Jurisdictions like the British Virgin Islands, the Cayman Islands, and the Isle of Man have robust AML frameworks. These jurisdictions have implemented strict measures to prevent illicit activities, mirroring international standards. Each jurisdiction has its specific guidelines and reporting requirements, which must be carefully reviewed.

Choosing a Bank

Opening an offshore bank account requires careful consideration, especially when selecting the right institution. Finding a reputable and stable bank is paramount to protecting your assets and ensuring smooth transactions. This section will guide you through the process of selecting an offshore bank, considering crucial factors such as reputation, services, fees, and regulatory compliance.

Reputable Offshore Banks

Selecting a reputable offshore bank is critical to the success of your financial endeavors. Thorough research is essential to identify banks with a strong track record and a proven commitment to client security. Banks with a long history, positive customer reviews, and a robust compliance framework are more likely to provide a safe and reliable platform for your financial needs.

Comparing Offshore Bank Services

Different offshore banks cater to diverse needs. Understanding the specific services offered by each bank is vital. Some banks might excel in investment management, while others might specialize in providing straightforward account maintenance. Compare the services, such as account types, international transfer capabilities, and investment products, to determine the best fit for your circumstances.

Factors to Consider When Selecting an Offshore Bank

Several factors influence the selection of an offshore bank. Beyond the services offered, consider the bank’s reputation, customer service, and financial stability. A bank with a positive track record and a history of strong financial performance is a valuable asset. Investigate the bank’s customer service responsiveness and efficiency to assess its potential for handling your needs. Thorough research into the bank’s history, including its financial stability and regulatory compliance, is crucial.

Importance of Researching Bank History and Financial Stability

The stability of an offshore bank is a key determinant of its suitability. A bank with a solid history and proven financial stability offers greater security for your funds. Investigate the bank’s financial reports, regulatory compliance, and any news or reports related to its performance. Assess the bank’s capital adequacy, profitability, and solvency ratios to gauge its financial strength.

Table Comparing Offshore Banks

| Bank Name | Services Offered | Fees (per annum/transaction) | Customer Reviews | Financial Stability Rating |

|---|---|---|---|---|

| Bank A | Investment accounts, foreign exchange, international transfers | $500 annual maintenance, $25 per transaction | Mostly positive, mentioning good customer service | Excellent |

| Bank B | Basic accounts, high-yield savings accounts | $250 annual maintenance, no transaction fees | Mixed reviews, some complaints about slow customer service | Good |

| Bank C | Trust services, asset protection | $750 annual maintenance, $50 per transaction | Very positive, emphasizing personalized service | Excellent |

Note: This table is for illustrative purposes only and does not represent an exhaustive comparison. Always conduct thorough research before selecting any bank.

Outcome Summary

Opening an offshore bank account is a significant decision, and this guide has served as your comprehensive resource. We’ve covered the essential aspects, from initial understanding to the final steps of account setup. Remember to thoroughly research, understand the implications, and seek professional advice when necessary. This detailed analysis equips you with the knowledge to make a well-informed choice.

FAQ

What are the common misconceptions surrounding offshore accounts?

Many people believe offshore accounts are inherently linked to tax evasion. However, offshore accounts can be legitimate tools for tax optimization, but only when used legally and in compliance with local and international regulations. Furthermore, it’s crucial to understand the legal implications in your specific jurisdiction.

What documents are typically required for account opening?

Essential documents often include a valid passport, proof of address, and potentially tax documentation. The exact requirements can vary significantly based on the specific offshore jurisdiction and the bank you choose. It’s wise to confirm these requirements directly with the bank.

What are the potential tax consequences of non-compliance?

Non-compliance with tax regulations surrounding offshore accounts can lead to severe penalties and legal repercussions. It’s crucial to consult with a qualified tax professional to understand the specific implications of your situation. This is paramount for avoiding potential issues down the road.

What is the role of KYC (Know Your Customer) procedures in offshore banking?

KYC procedures are essential for verifying the identity of account holders. Offshore banks are required to comply with these procedures, which help prevent money laundering and other financial crimes. It is a critical aspect of maintaining regulatory compliance.

Leave a Reply