Opening an overseas bank account can unlock a world of financial opportunities, but navigating the complexities of international banking can feel daunting. This comprehensive guide breaks down the process, from understanding the various account types to managing funds across borders. We’ll cover everything you need to know about opening an overseas bank account, including potential benefits, risks, and the crucial steps involved.

From comparing different bank options to understanding regional regulations, we’ll equip you with the knowledge to make informed decisions. We’ll delve into the paperwork, fees, and crucial considerations for a smooth and successful experience.

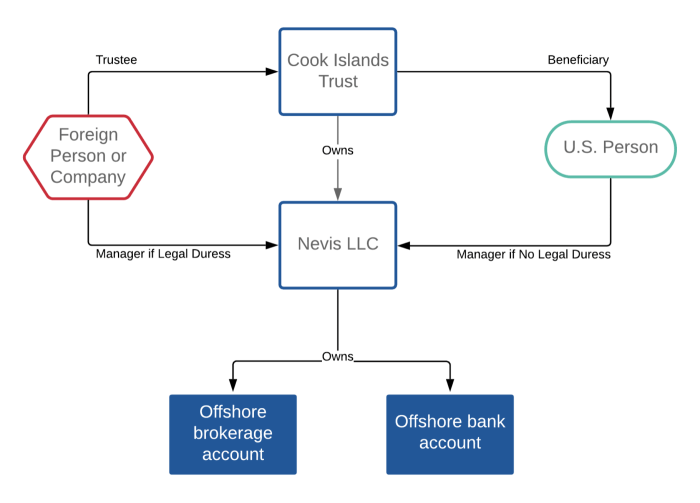

Introduction to Overseas Bank Accounts

Source: bancoli.com

An overseas bank account, sometimes referred to as an international bank account, is a financial account held at a bank located outside of your home country. These accounts offer unique features and potential advantages, but also carry certain risks and complexities. Understanding these nuances is crucial for making an informed decision about whether or not an overseas bank account is suitable for your financial goals.Understanding the different types of overseas bank accounts available is key to making the right choice.

These accounts cater to various financial needs, from everyday transactions to long-term investments. Exploring the benefits and drawbacks will help you determine if opening one aligns with your personal circumstances.

Types of Overseas Bank Accounts

Different types of overseas bank accounts cater to varying needs and goals. Each type has its own set of features, benefits, and drawbacks.

- Checking Accounts: Designed for frequent transactions, these accounts are ideal for everyday expenses and bill payments. They often offer debit card access and online banking features.

- Savings Accounts: These accounts are geared towards accumulating funds and earning interest. They often have lower transaction limits compared to checking accounts but offer higher interest rates, particularly in accounts offering foreign currency savings.

- Investment Accounts: These accounts are tailored for growing wealth through investment options. They can include brokerage accounts, money market accounts, or certificates of deposit (CDs). Specific investment vehicles may offer varying levels of risk and potential returns.

Potential Benefits of Overseas Bank Accounts

Opening an overseas bank account can present several potential advantages.

Opening an overseas bank account can be a complex process, requiring careful consideration of various factors. Understanding the nuances of offshore banking is crucial, and a detailed comparison of different offshore bank account options can greatly aid the process. For a comprehensive overview of the available options, check out this offshore bank account comparison. Ultimately, selecting the right overseas bank account depends on your specific financial needs and goals.

- Tax Advantages: Depending on the jurisdiction and your individual circumstances, an overseas bank account might offer opportunities for tax optimization. This could involve utilizing specific tax treaties or structuring your finances to minimize tax liabilities. However, tax laws are complex and vary significantly by country and individual circumstances, so professional guidance is essential.

- Higher Interest Rates: Some overseas banks offer higher interest rates on savings and investment accounts compared to domestic banks. This can lead to faster accumulation of savings and returns on investments. However, this advantage is not universal and varies greatly by bank and market conditions.

- Currency Exchange Opportunities: If you engage in international transactions or hold assets denominated in different currencies, an overseas bank account can provide opportunities for currency exchange. This can be beneficial for managing foreign exchange risk and maximizing your returns.

Potential Drawbacks of Overseas Bank Accounts

Opening an overseas bank account also comes with potential downsides.

Opening an overseas bank account can unlock opportunities, but understanding the nuances is key. Offshore banking, for example, often involves setting up accounts in jurisdictions outside your home country, and what is offshore banking can impact tax implications and regulations. Ultimately, researching the specifics of each overseas bank account is crucial for making informed decisions.

- Compliance Issues: Navigating the regulations and compliance requirements of different jurisdictions can be complex. Failure to comply with local laws and regulations could result in penalties or other legal issues.

- Currency Exchange Risks: Fluctuations in exchange rates can impact the value of your funds when converting between currencies. Understanding and managing these risks is crucial to minimizing potential losses.

- Potential for Additional Fees: Fees associated with overseas banking can vary significantly. These could include account maintenance fees, transaction fees, or currency conversion fees. Understanding the fees upfront is important.

Comparison of Overseas Bank Account Types

The following table provides a comparative overview of various overseas bank account types.

| Account Type | Features | Pros | Cons |

|---|---|---|---|

| Checking | Frequent transactions, debit card access, online banking | Ease of use for everyday expenses, convenient access to funds | Potentially lower interest rates compared to savings, limited investment options |

| Savings | Accumulating funds, earning interest, usually lower transaction limits | Higher interest rates than checking, suitable for building savings | Less flexibility for frequent transactions, potentially lower interest rates compared to investment accounts |

| Investment | Investment options like brokerage accounts, money market accounts, CDs | Potential for higher returns through investment vehicles, tailored for wealth growth | Higher risk associated with investment options, more complex to manage |

Requirements and Procedures

Opening an overseas bank account involves a meticulous process. Understanding the necessary documents, verification procedures, and steps involved is crucial for a smooth transaction. This section details the requirements and procedures for successfully establishing an overseas bank account.Thorough preparation and adherence to the bank’s specific guidelines are vital to avoid delays and complications. Different banks may have slightly varying requirements, so it’s essential to carefully review the bank’s guidelines before initiating the process.

Essential Documents

A comprehensive list of documents is typically required for account opening. These documents serve as proof of identity, address, and financial standing. Failure to provide accurate and complete documentation can result in account application rejection.

- Passport: A valid passport is usually required to verify identity. It serves as a primary identification document. Ensure the passport is valid for the duration of your intended stay and that copies of the passport pages are provided as needed.

- Proof of Address: Documents demonstrating your current residential address are necessary. These could include utility bills, bank statements, or lease agreements. Recent documents within the last three months are usually preferred.

- Proof of Income: Depending on the bank and account type, you might need to provide proof of income. This can be in the form of pay stubs, tax returns, or employment contracts. The specific requirements will vary.

- Other Documents: Additional documents like a driver’s license, national ID card, or marriage certificate might be needed, depending on the country and bank. It’s wise to check with the bank in advance about the specific documents they require.

Identity Verification Processes

Banks employ robust identity verification measures to mitigate risks and comply with regulations. These processes help ensure the account holder’s authenticity.

- Know Your Customer (KYC): KYC procedures are standard practice. These involve verifying the account holder’s identity, address, and other relevant information to prevent fraud. This process might involve online verification, physical verification at the bank, or a combination of both.

- Anti-Money Laundering (AML): AML procedures are also critical. These measures aim to prevent the use of the account for illegal activities. AML checks might involve reviewing transaction patterns and other activities related to the account.

- Enhanced Due Diligence (EDD): In some cases, enhanced due diligence measures might be applied, particularly for high-value accounts or accounts in high-risk jurisdictions. EDD processes often involve more stringent verification procedures to ensure compliance with regulations.

Account Opening Process

The account opening process typically follows a structured sequence. A clear understanding of the process will help expedite the application.

- Application: Complete the account application form accurately. Provide all requested information, including personal details, financial information, and any required supporting documents.

- Document Submission: Submit the required documents to the bank. Ensure all documents are properly formatted and in the correct order. Use secure methods to submit documents, if available.

- Verification: The bank will verify your identity and other details. This process might take a few days or weeks, depending on the bank’s procedures.

- Account Activation: Once the verification is complete, your account will be activated. You will receive notification from the bank regarding account activation.

- Account Access: After activation, you can access your account and use it for transactions.

Typical Documentation Requirements

The table below Artikels common documentation requirements for opening an overseas bank account. Always check with the specific bank for their exact requirements.

| Document Type | Description | Purpose |

|---|---|---|

| Passport | A valid passport issued by the applicant’s country of origin. | Proof of identity and nationality. |

| Proof of Address | Recent utility bills, bank statements, or lease agreements. | Verification of current residential address. |

| Proof of Income | Pay stubs, tax returns, or employment contracts. | Verification of income and financial standing. |

| Other Documents | Driver’s license, national ID card, marriage certificate, or other relevant documents. | Additional verification of identity, address, or relationship. |

Factors to Consider: Opening An Overseas Bank Account

Opening an overseas bank account involves more than just signing paperwork. Careful consideration of various factors is crucial for a smooth and profitable experience. This section delves into the key aspects you need to evaluate before committing to a particular bank.The landscape of overseas banking is diverse, offering a range of options for different needs and situations. Choosing the right bank can significantly impact your financial well-being, from managing your international transactions to navigating complex regulatory environments.

Understanding these factors empowers you to make informed decisions and avoid potential pitfalls.

Comparing Overseas Bank Offerings

Different banks cater to various customer segments. Thoroughly researching and comparing options is vital to finding a bank that aligns with your specific requirements. Consider factors such as account types, fees, and available services. A comprehensive comparison helps you choose a bank that provides the necessary functionalities without excessive costs.

Selecting a Bank: Key Criteria

Selecting an overseas bank requires careful evaluation of numerous criteria. Crucial factors include fees (monthly maintenance, transaction fees, foreign exchange rates), customer service quality (response times, accessibility, and support channels), and the bank’s reputation and stability. These elements directly impact the overall banking experience.

Regulatory Environment in the Target Country

Understanding the regulatory environment in the target country is essential. Laws and regulations regarding foreign accounts can significantly influence account management. Thorough research into local banking laws, including those related to foreign exchange, taxation, and sanctions, is crucial. This knowledge safeguards you from unforeseen complications.

Implications of International Banking Regulations

International banking regulations can have various implications for managing your account. These regulations often impose specific reporting requirements for certain transactions and account activities. Understanding these implications helps you navigate account management efficiently and avoid potential issues with compliance.

Tax Implications of Overseas Accounts

Tax implications associated with overseas accounts vary significantly depending on your jurisdiction and the specific banking structure. Thorough consultation with a tax advisor is highly recommended. They can provide personalized guidance on the tax implications of your specific circumstances. Different jurisdictions have different tax rules for international transactions and account ownership. Understanding these differences is crucial for effective tax planning.

Examples of Bank Fees

Bank fees vary considerably. For instance, monthly maintenance fees can range from negligible to substantial amounts. Transaction fees, foreign exchange rates, and other charges can vary greatly between banks. Analyzing fee structures allows you to compare and select a bank that best fits your budget and needs. For example, one bank might charge 1.5% on currency conversions, while another might charge 0.5%.

These small differences can significantly impact your overall financial outcome over time.

Managing Foreign Currency Exchange

Managing foreign currency exchange effectively is critical for overseas banking. Understanding exchange rates, fees associated with conversions, and the various available options for managing currency fluctuations is essential. This process can involve using a bank’s in-house exchange platform or utilizing third-party services. Thorough research and comparison of foreign exchange services can help minimize potential losses. Be sure to understand the potential implications of different exchange rates on your transactions.

Opening an Account in Specific Regions

Source: offshorelivingletter.com

Opening an overseas bank account involves navigating diverse regulations and procedures across different regions. Understanding these nuances is crucial for a smooth and successful account opening process. Different countries have varying compliance requirements, impacting the documentation needed, the time frame for approval, and potential fees. This section delves into the specifics of opening accounts in key regions, offering insights into the challenges and advantages of each location.

Opening an overseas bank account can unlock various financial opportunities, but navigating the process can be tricky. A prime example of this is opening a bank account in Jersey, a popular offshore financial center, opening a bank account in jersey. Understanding the specific regulations and procedures for this type of account is crucial for a smooth and successful experience when considering an overseas bank account.

Account Opening Nuances in Europe

European regulations for banking are generally stringent and focused on consumer protection. Compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures is paramount. The specific documentation requirements and verification processes vary between European Union member states. For instance, obtaining a local address or proof of residency might be essential. The account opening process often involves multiple verification steps, potentially extending the timeframe for approval.

Account Opening Nuances in Asia

Asia presents a diverse landscape with varied banking regulations across different countries. Some Asian nations have stricter regulations regarding foreign account ownership, while others are more open to international banking. The process for opening an account can differ significantly based on the country. For example, in some Asian countries, a physical presence might be required during the account opening process, while others may allow for remote opening.

Language barriers and cultural nuances may also influence the account opening procedure.

Account Opening Nuances in North America

North American regulations generally align with international standards, focusing on AML and KYC compliance. The specific requirements for opening an account vary between countries. For example, the United States requires rigorous documentation to establish identity and source of funds. Account opening processes in North America are often streamlined and efficient compared to other regions, but specific regulations still apply.

Comparative Analysis of Account Opening Procedures

| Region | Key Regulations | Account Opening Steps | Typical Fees |

|---|---|---|---|

| Europe | Strict KYC/AML compliance; varying regulations across EU member states; focus on consumer protection | Multiple verification steps; potentially lengthy process; local address verification often required | Likely higher account maintenance fees and potentially higher opening fees; fees may vary by bank |

| Asia | Varying regulations across countries; some countries have stricter foreign account ownership rules; physical presence may be required | Process may differ greatly by country; potential for longer processing time; language barriers and cultural considerations may be relevant | Fees can range from low to high; may depend on the specific bank and country |

| North America | Generally aligned with international standards; rigorous documentation required; focus on AML and KYC compliance | Streamlined process compared to other regions; often efficient but specific regulations apply | Likely lower opening fees compared to Europe; potential for account maintenance fees |

Pros and Cons of Opening an Account in Specific Regions, Opening an overseas bank account

Careful consideration of the advantages and disadvantages of opening an account in a specific region is crucial. Different regions offer varying benefits, from lower account maintenance fees to greater access to financial services. Analyzing the potential drawbacks, such as strict regulations and lengthy procedures, is also essential.

Maintaining an Overseas Bank Account

Managing an overseas bank account effectively involves careful planning and proactive management. Understanding the nuances of international transactions, potential challenges, and the available tools is crucial for a smooth experience. This section delves into the practical aspects of maintaining your account, from transferring funds to resolving issues.

Methods for Managing Funds

Efficiently managing funds in your overseas account hinges on utilizing available tools and services. This includes leveraging online banking platforms, mobile apps, and potentially, physical branches if accessible. The ease of access and control varies greatly depending on the bank and the specific account type. Familiarity with these tools is essential for seamless fund management.

International Fund Transfer Processes

International fund transfers are a core component of overseas account management. Understanding the various transfer methods, their associated fees, and the timeframes involved is crucial for successful transactions. Choosing the most suitable method depends on factors such as the destination, transaction amount, and speed requirements. Different methods offer varying degrees of speed and cost-effectiveness.

Common Challenges Faced by Account Holders

Account holders frequently encounter challenges during the maintenance process. These can range from issues with international transfers to difficulties accessing online banking services. Currency fluctuations, exchange rate variations, and unexpected transaction fees can also impact account management. Understanding these potential pitfalls and proactively addressing them is vital for a positive experience.

Resolving Account-Related Issues

Prompt and effective resolution of account-related problems is paramount. Knowing the steps to resolve common issues, such as blocked transactions or incorrect information, can significantly reduce frustration and maintain account health. The availability of customer support channels, including phone, email, and online chat, can be instrumental in navigating these situations. Always keep accurate records of transactions and correspondence.

Utilizing Online Banking Services

Online banking services are indispensable for managing overseas accounts. These services often provide a comprehensive overview of account activity, including transaction history, balance details, and pending transfers. They allow for convenient fund transfers, bill payments, and account monitoring from anywhere with internet access. Understanding the security features of these platforms is also important.

Table of Different Fund Transfer Methods

| Transfer Method | Description | Pros | Cons |

|---|---|---|---|

| Wire Transfer | A traditional method involving transferring funds through a network of banks. | Generally reliable and widely accepted. | Can be slower than other methods, often involves higher fees. |

| Electronic Transfer | Funds are transferred electronically between bank accounts. | Faster and often more affordable than wire transfers. | May be less reliable in some situations; security risks can arise. |

| International Money Transfer Services (e.g., Western Union, MoneyGram) | Third-party services facilitate transfers to specific destinations. | Convenient for sending money to unbanked individuals. | Higher fees compared to bank transfers. |

Illustrative Examples

Source: certified-translation.us

Opening an overseas bank account can seem daunting, but with careful planning and research, it can be a valuable financial tool. This section provides real-world examples to illustrate the process, highlighting both successes and potential challenges. Understanding these scenarios empowers you to make informed decisions.

Case Study: A Successful Overseas Bank Account Opening

A tech entrepreneur, based in the US, needed a European bank account for international business transactions. They researched several banks, considering factors like fees, transaction limits, and customer service. Choosing a bank with strong international remittance capabilities was crucial. They opted for a bank with a strong presence in their target markets, and this choice proved advantageous in terms of efficiency and cost-effectiveness.

Opening an overseas bank account can be a complex process, but finding the right platform to do it online makes it significantly easier. Many providers offer a streamlined approach for opening foreign bank accounts online, simplifying the whole procedure. This can save you valuable time and effort, especially when considering opening an overseas bank account. open foreign bank account online solutions are becoming increasingly popular for a reason.

The key to successful account opening lies in choosing a reputable provider and understanding the specific requirements for your desired location.

The entrepreneur followed the bank’s account opening procedures meticulously, providing all necessary documentation promptly. This proactive approach ensured a smooth and rapid account opening process.

Overseas Bank Account Management Scenario

Managing an overseas bank account involves regular monitoring of transactions and account balances. Maintaining accurate records of transactions, both incoming and outgoing, is vital for preventing errors and facilitating tax compliance. Utilizing online banking platforms for managing account activity is highly recommended for its efficiency and convenience. Regularly reviewing account statements, noting any unusual activity, and promptly addressing any discrepancies are essential for maintaining the security and integrity of the account.

Steps to Close an Overseas Bank Account

Closing an overseas bank account often involves a specific procedure, which varies between banks and jurisdictions. This procedure typically requires submitting a formal request to the bank, providing supporting documentation, and potentially closing related accounts. Crucially, it is essential to understand the bank’s specific requirements and timelines. Clearing all outstanding transactions and ensuring the closure of linked accounts is vital to avoid any future complications.

Implications of Closing an Overseas Account

Closing an overseas account may have implications for various aspects of your financial life. You may need to adjust your international payment systems and consider the tax implications of closing the account, especially if it’s been used for business transactions. It is crucial to consult with a financial advisor to understand the potential tax implications and ensure compliance with regulations in both your home country and the country where the account was held.

Scenario: Common Issues and Solutions

A frequent issue encountered is delays in account opening due to incomplete or incorrect documentation. Carefully reviewing and verifying the required documents is crucial for avoiding these delays. The solution involves double-checking all information provided and ensuring accurate translations if needed. A proactive approach to document verification will significantly reduce the likelihood of issues. Other common problems include currency exchange rate fluctuations and high transaction fees.

Diversifying payment options and utilizing online tools for tracking exchange rates are effective solutions.

Final Review

In conclusion, opening an overseas bank account can be a powerful financial tool, but it’s essential to thoroughly research your options and understand the associated risks and rewards. This guide has provided a framework for understanding the process, from initial research to ongoing account management. Remember to prioritize your financial goals and conduct thorough due diligence before making any commitments.

Ultimately, your choice should align with your specific financial needs and risk tolerance.

FAQ Insights

What are the common fees associated with opening and maintaining an overseas bank account?

Fees vary significantly depending on the bank and account type. Opening fees, monthly maintenance fees, international transaction fees, and currency exchange fees are all potential costs to consider. It’s crucial to compare these fees across different banks to find the best option for your needs.

What are the tax implications of holding an overseas bank account?

Tax implications are complex and vary based on your location, the bank’s jurisdiction, and your specific financial situation. Consult with a qualified tax advisor to understand the potential tax liabilities associated with holding an overseas bank account.

What are the common challenges faced by overseas bank account holders?

Common challenges include navigating foreign regulations, managing currency exchange fluctuations, and resolving issues with international transactions. Understanding these potential issues can help you plan for them and mitigate their impact.

How can I securely transfer funds internationally using an overseas bank account?

Use reputable transfer services, check for hidden fees, and be aware of potential security risks. Utilize secure online banking platforms whenever possible to minimize risk.

Leave a Reply