Easiest offshore bank account to open? This in-depth guide unravels the complexities of establishing an offshore banking presence. We’ll explore the motivations, factors influencing ease, and key jurisdictions to consider, helping you navigate the process effectively and confidently.

Choosing the right offshore bank account is a crucial financial decision. Understanding the various types of accounts, associated benefits and drawbacks, and the critical KYC (Know Your Customer) procedures will empower you to make an informed choice. This comprehensive resource provides a roadmap to opening an offshore account with minimal hassle and maximum clarity.

Introduction to Offshore Bank Accounts

Source: nomadcapitalist.com

Offshore bank accounts are financial accounts held in a country different from the account holder’s primary residence. These accounts offer a range of potential benefits, but also come with inherent complexities and potential risks. Understanding the motivations, differences, and key considerations is crucial before opening such an account.Opening an offshore account is often driven by a desire for tax optimization, asset protection, or financial privacy.

Individuals and businesses may seek to reduce their tax burden by holding assets in jurisdictions with lower or different tax rates. Asset protection strategies aim to shield assets from legal claims or creditors. Maintaining financial privacy can be important for those seeking to keep their financial affairs confidential. It’s crucial to note that the specific benefits and implications vary based on individual circumstances and local regulations.

Motivations Behind Opening an Offshore Account

A primary motivation behind opening an offshore account is tax optimization. Different countries have varying tax rates and regulations, potentially allowing individuals or businesses to reduce their overall tax liability. Asset protection is another significant driver. Offshore accounts can help shield assets from creditors or legal disputes. Furthermore, financial privacy is often sought, allowing individuals or entities to keep their financial transactions and holdings confidential.

These motivations, however, must be balanced against potential legal and regulatory ramifications.

Key Differences Between Offshore and Domestic Bank Accounts

Offshore accounts differ significantly from domestic accounts in terms of regulations, accessibility, and fees. Offshore banks often operate under different legal frameworks, which can affect the accessibility and use of the accounts. Additionally, regulatory oversight may differ, impacting the level of transparency and compliance required. Account opening procedures and documentation requirements may vary substantially. While domestic accounts are generally subject to domestic tax laws and reporting requirements, offshore accounts often operate outside these parameters, leading to potential complications in reporting and compliance.

Comparison of Key Features

| Feature | Offshore Bank Account | Domestic Bank Account |

|---|---|---|

| Account Opening Requirements | Often more extensive, including extensive documentation, verification processes, and potentially legal counsel. | Generally simpler, requiring basic identification and financial information. |

| Fees | May include higher account maintenance fees, potentially higher transaction fees, and variable charges depending on the specific bank and services utilized. | Typically have lower account maintenance fees, transaction fees, and more predictable charges. |

| Accessibility | May require more effort for account access and transactions due to geographical location and different banking regulations. | Accessible and easy to manage through online banking, ATMs, and physical branches, providing greater convenience. |

| Tax Implications | Tax implications can be complex and depend heavily on the specific jurisdiction, often requiring careful tax planning and consulting with experts. | Tax implications are generally straightforward and governed by domestic tax laws. |

Factors Affecting Ease of Opening

Source: relinconsultants.com

Opening an offshore bank account is a complex process, influenced by numerous factors. Understanding these factors is crucial for anyone considering such a move, as they directly impact the overall experience and potential success of the endeavor. Choosing the right jurisdiction and adhering to the necessary regulations can significantly streamline the process.Navigating the nuances of different offshore jurisdictions is key to selecting the optimal location for your needs.

The legal and regulatory environments vary widely, impacting account opening procedures and the associated compliance requirements. This variability necessitates a thorough understanding of each jurisdiction’s unique characteristics to ensure a smooth and compliant account setup.

Nationality and Residency Requirements

Nationality and residency requirements play a significant role in the ease of account opening. Certain jurisdictions may have stricter rules for non-residents, potentially making the process more challenging. These rules vary across jurisdictions, and it’s crucial to research the specific regulations of each potential location. For example, some jurisdictions might prioritize residents, while others may have less stringent requirements for non-residents, but this is subject to the overall regulatory environment.

A thorough understanding of the requirements is essential for a successful outcome.

Account Type and Purpose

The type of account being opened can also affect the ease of opening. Different account types have varying requirements and documentation demands. A business account, for instance, may necessitate more extensive documentation than a personal account. Additionally, the intended purpose of the account—investment, business funding, or personal use—can also influence the required paperwork and processes. Consider the specific purpose of the account to identify the most suitable type.

Legal Frameworks in Offshore Jurisdictions

The legal frameworks in different offshore jurisdictions vary considerably. Jurisdictions with robust regulatory environments might have stricter account opening protocols to mitigate financial crime risks. Conversely, jurisdictions with less stringent regulations may present a quicker, but potentially riskier, path to account setup. The implications of varying legal frameworks need careful consideration, as they can affect the level of scrutiny applied during the account opening process.

Furthermore, the ongoing compliance requirements will also be influenced by the legal framework in place.

Due Diligence Processes

Due diligence processes are paramount in the offshore banking sector. These processes are crucial for verifying the identity and legitimacy of account holders and mitigating the risk of illicit activity. Thorough due diligence can vary across jurisdictions, demanding compliance with local regulations and international standards. Strong due diligence processes are vital for ensuring the legitimacy of the account and mitigating legal risks for all parties involved.

Role of Intermediaries

Intermediaries, such as financial advisors or offshore account specialists, can play a crucial role in facilitating the account opening process. These intermediaries often have extensive knowledge of the relevant jurisdictions and can navigate the complexities of the process more efficiently. They can also assist in gathering the necessary documentation and ensure compliance with all regulations. In some cases, using an intermediary can significantly reduce the time and effort required to open an offshore account.

Common Account Opening Requirements

| Jurisdiction | Nationality Requirements | Residency Requirements | Documentation Needed |

|---|---|---|---|

| Jurisdiction A | No specific requirements | Proof of residence for 3 months | Passport, utility bill, employment contract |

| Jurisdiction B | Must be a citizen of a specific country | Proof of residence for 6 months | Passport, tax returns, bank statements |

| Jurisdiction C | No restrictions | No residency requirement | Passport, business registration documents |

This table provides a simplified overview of common account opening requirements. It is crucial to consult the specific regulations of each jurisdiction for accurate and up-to-date information. Furthermore, specific account types may necessitate additional or different documentation.

Comparing Offshore Jurisdictions

Choosing the right offshore jurisdiction for your bank account is crucial for minimizing risks and maximizing benefits. Different jurisdictions offer varying levels of regulatory oversight, tax implications, and ease of account opening. Understanding these nuances is key to making an informed decision.Offshore banking jurisdictions are often compared based on their regulatory environments, secrecy laws, and overall reputation for financial stability.

This comparison reveals how different jurisdictions approach financial transparency and client confidentiality, ultimately impacting the ease of opening and maintaining an account.

Regulatory Environments and Account Opening Procedures

The regulatory landscape significantly impacts the ease of opening an offshore bank account. Stricter regulations often mean more rigorous due diligence processes, potentially increasing the time and effort required for account setup. Conversely, less stringent regulations may pose risks related to financial stability and potential compliance issues. Understanding the regulatory environment is vital to assess the potential hurdles and ensure compliance.

Reputable Offshore Banking Jurisdictions

Several jurisdictions are renowned for their favorable regulatory environments and established financial infrastructure. These jurisdictions have a track record of maintaining stability and offer a range of banking services. The reputation of a jurisdiction plays a crucial role in the overall experience and security of offshore banking.

- British Virgin Islands (BVI): Known for its well-established financial sector and streamlined procedures, the BVI often attracts businesses seeking a balance between security and efficiency. The jurisdiction’s robust legal framework fosters trust and facilitates smooth account opening processes.

- Cayman Islands: A popular choice for its robust regulatory framework and low tax rates, the Cayman Islands offers a reliable and efficient banking environment. The jurisdiction is often praised for its transparency and stability, making it attractive for international businesses and high-net-worth individuals.

- Nevis: The Nevis International Financial Services Association (NIFS) provides a stable and secure environment for offshore banking. Nevis’s financial regulations and the presence of international financial institutions contribute to its attractiveness for offshore account holders.

- Hong Kong: A major international financial center, Hong Kong offers a blend of accessibility and advanced banking infrastructure. The jurisdiction’s established legal framework and strong financial standing contribute to its appeal.

Pros and Cons of Different Jurisdictions

Evaluating the pros and cons of each jurisdiction is essential for a tailored approach to offshore banking. This assessment should consider the specific needs and goals of the individual or entity seeking an offshore account.

| Jurisdiction | Pros | Cons |

|---|---|---|

| British Virgin Islands | Streamlined account opening, robust legal framework, well-established financial sector. | Potential for increased scrutiny from regulatory bodies in certain cases. |

| Cayman Islands | Reliable and efficient banking environment, low tax rates, robust regulatory framework. | May face stricter due diligence requirements compared to some other jurisdictions. |

| Nevis | Stable and secure environment, favorable regulatory regime, international financial services association. | Limited banking infrastructure compared to larger offshore hubs. |

| Hong Kong | Major international financial center, advanced banking infrastructure, accessibility. | May not be as tax-favorable as other jurisdictions. |

Account Types and Their Implications

Choosing the right offshore bank account type is crucial for maximizing benefits and minimizing potential risks. Understanding the nuances of different account types—from personal accounts to investment vehicles—is essential for making an informed decision. Different accounts cater to diverse needs, and the ease of opening can vary significantly based on the specific type.Offshore bank accounts are not a one-size-fits-all solution.

Factors like your financial goals, regulatory environment, and personal circumstances all play a significant role in determining the optimal account type. Navigating the landscape of offshore accounts requires careful consideration of the various options available.

High-Yield Savings Accounts

High-yield savings accounts offer attractive interest rates compared to traditional domestic accounts. These accounts can be a valuable tool for maximizing returns on deposited funds, but opening them might involve additional requirements and scrutiny, especially when linked to international transactions. Factors such as minimum balance requirements and transaction limits can affect the ease of opening and using these accounts.

While exploring the easiest offshore bank accounts to open, it’s crucial to understand the nuances surrounding offshore banking. This often leads to questions about the best offshore banks to hide money, which can be a sensitive topic. Ultimately, the easiest offshore bank account to open might not align with your goals if secrecy is a primary concern. You should carefully consider the implications of opening an offshore account and research options like those mentioned in best offshore banks to hide money.

Choosing the right account will depend on your individual circumstances.

Investment Accounts

Investment accounts are tailored for individuals looking to grow their capital through investments in stocks, bonds, or other financial instruments. They often come with investment management services and potentially more stringent KYC (Know Your Customer) requirements. The complexity of these accounts can impact the opening process, and the associated fees and commissions should be thoroughly reviewed. Some accounts may require a higher initial investment or minimum balance to qualify.

Personal Accounts

Personal accounts provide a platform for managing personal finances and transactions. The process of opening a personal account can be straightforward for some jurisdictions and more involved for others, potentially depending on the required documentation and the bank’s specific policies. Factors such as the account’s intended use, the required documentation, and the bank’s specific policies can affect the ease of opening and ongoing management.

These accounts can serve as a cornerstone for managing personal funds offshore.

Business Accounts

Business accounts are designed for companies and other legal entities to conduct business activities and manage funds. Opening a business account typically involves a more extensive due diligence process, demanding detailed documentation of the business’s operations and legal structure. The required documentation and verification processes can significantly impact the time and effort required to open a business account.

Table: Account Types and Implications

| Account Type | Ease of Opening | Benefits | Drawbacks |

|---|---|---|---|

| High-Yield Savings | Moderate (often higher scrutiny) | Higher interest rates | Potential minimum balance requirements, specific transaction rules |

| Investment | Moderate to High (depends on complexity) | Investment management, potentially higher returns | Stricter KYC, potentially higher fees and commissions |

| Personal | Variable (depending on jurisdiction and bank) | Convenient management of personal funds | Limited investment options, may not offer high-yield interest |

| Business | High (extensive documentation needed) | Dedicated for business transactions | Time-consuming due diligence process, often higher fees |

Understanding the Role of KYC

Opening an offshore bank account often involves a rigorous process, and a crucial component of this process is Know Your Customer (KYC) compliance. This ensures that the bank adheres to anti-money laundering (AML) regulations and reduces the risk of illicit activity. Navigating these requirements can be tricky, especially for those unfamiliar with offshore banking. Understanding the KYC process, the potential challenges, and the jurisdictional variations is essential for a smooth and compliant account opening.KYC procedures for offshore accounts are designed to verify the identity and background of the account holder.

This verification process helps banks identify and mitigate risks associated with financial crime. Failure to meet these requirements can result in account rejection or even legal repercussions for both the account holder and the bank. A thorough understanding of these procedures and potential obstacles is crucial for a successful offshore banking experience.

KYC Procedures for Offshore Accounts

KYC procedures for offshore accounts typically involve verifying the identity of the account holder. This verification often extends beyond basic information to include supporting documentation to confirm the information provided. Banks frequently request detailed information about the account holder’s business activities and sources of funds. The thoroughness of the verification process varies significantly depending on the jurisdiction and the specific bank.

Potential Challenges in Satisfying KYC Requirements

Satisfying KYC requirements can present various challenges, particularly for those unfamiliar with the intricacies of offshore banking. Gathering the necessary documentation, particularly for individuals or entities with complex financial structures, can be time-consuming and potentially problematic. The required documents and their format can also vary significantly between jurisdictions, making compliance challenging. The complexity of the process can be daunting, especially for those operating internationally.

Variations in KYC Protocols Across Jurisdictions

KYC protocols differ considerably among offshore jurisdictions. Some jurisdictions may have more stringent requirements than others. This variation can impact the ease of opening an account, as the documentation needed and the verification procedures vary considerably. For example, a jurisdiction known for its lax regulations may require less stringent documentation compared to one with more stringent anti-money laundering (AML) laws.

This difference in protocols should be carefully considered when selecting a jurisdiction for an offshore account.

Common KYC Documents Requested by Offshore Banks

The following list provides a common sample of KYC documents requested by offshore banks:

- Passport or national ID card: This provides proof of identity and nationality.

- Proof of address: This can include utility bills, bank statements, or lease agreements, demonstrating the account holder’s current residence.

- Proof of income: This may involve tax returns, pay stubs, or business financial statements, demonstrating the account holder’s financial situation.

- Business registration documents (if applicable): These are necessary for business accounts and might include articles of incorporation, business licenses, or tax registration documents.

- Supporting documents for unusual transactions: In cases of large or unusual transactions, further verification of the funds’ origin is frequently required.

Understanding the specific requirements for each jurisdiction and bank is critical to a smooth account opening process. These documents are frequently required to comply with AML and KYC regulations, thereby mitigating risks and ensuring compliance.

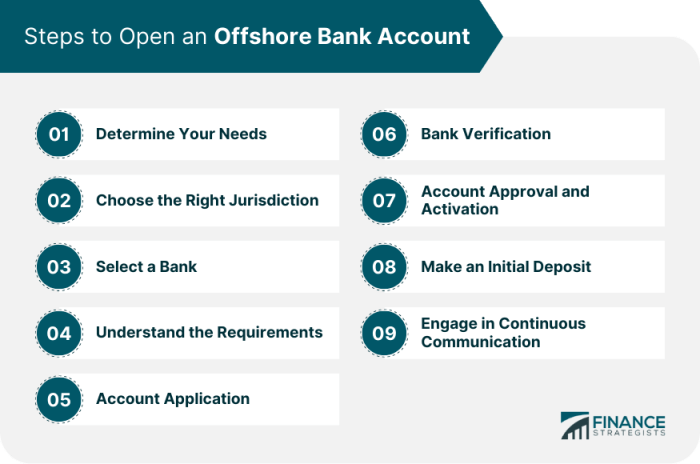

Navigating the Application Process

Opening an offshore bank account isn’t a simple task. It requires careful preparation, understanding of regulations, and a clear grasp of the specific requirements of each jurisdiction. Thorough research and a methodical approach are key to a smooth application process. This section will guide you through the steps involved, outlining necessary documents and providing examples of typical application forms.

Step-by-Step Account Opening Procedure

The process generally follows a similar pattern across jurisdictions, but nuances exist. A common thread is the rigorous verification procedures, which are designed to mitigate risks and comply with international regulations.

Looking for the easiest offshore bank account to open? Understanding what offshore banking actually entails is key. Offshore banking, essentially, involves establishing a bank account in a country different from your primary residence, often for financial management and investment strategies. To find the easiest offshore bank account to open, you need to thoroughly research and compare different providers.

what is offshore banking to get a better grasp of the concept. Different factors, such as regulations and fees, can impact the ease of opening such an account.

- Preliminary Research and Due Diligence: Thoroughly investigate the chosen offshore jurisdiction’s regulations and the specific bank’s requirements. Understanding the legal framework and the bank’s policies is critical. This step includes verifying the bank’s reputation and financial stability.

- Account Type Selection: Determine the type of account best suited to your needs. Consider factors like currency, account maintenance fees, and access restrictions. Different account types will have varying application processes and documentation needs.

- Gathering Required Documents: Compile all necessary documentation. This often includes proof of identity, address verification, and financial information. A checklist is crucial to avoid omissions.

- Completing the Application Form: Carefully fill out the application form, providing accurate and complete information. Any discrepancies may lead to delays or rejection.

- Submitting Documents and Application: Submit the completed application form and all supporting documents to the bank. Ensure all submissions are accurate and in the correct format. Double-check for completeness before sending.

- Verification and Approval: The bank will verify your identity and the documents provided. This process can take several days or weeks. Keep in touch with the bank if you have not received any updates. Follow-up is important.

- Account Activation and Access: Once approved, your account will be activated. The bank will provide instructions on how to access your account and manage it.

Necessary Documents and Information, Easiest offshore bank account to open

The specific documents required vary depending on the jurisdiction and account type. However, some common requirements include:

- Proof of Identity: Passport, national ID card, driver’s license. These documents serve as primary evidence of your identity.

- Proof of Address: Utility bills, bank statements, lease agreements. These documents verify your current residential address.

- Financial Information: Bank statements, tax returns, proof of income. The type and level of financial information required depend on the account type and the bank’s policies.

- References (as needed): Letters of recommendation or references from a trusted source. In certain cases, providing references can enhance the application process.

- Power of Attorney (as needed): If applying on behalf of another party, a Power of Attorney document is essential.

Examples of Application Forms

Unfortunately, providing precise examples of application forms for various account types is not possible in this context. The forms vary significantly based on the bank and the account type. Directly contacting the bank you’re interested in will yield the most accurate information.

Visualizing the Account Opening Process

A flowchart would best illustrate the entire account opening process. However, creating such a graphic is beyond the scope of this text. The process generally follows a sequential pattern, starting with research and ending with account activation.

Assessing Reputation and Reliability

Opening an offshore bank account can be tempting, but it’s crucial to ensure the institution’s reputation and reliability. Just because a bank is offshore doesn’t automatically mean it’s trustworthy. Thorough due diligence is paramount to avoiding potential scams and ensuring your financial security. This process involves researching the bank’s history, financial stability, and regulatory compliance.Offshore banking jurisdictions often have varying degrees of regulatory oversight.

Some jurisdictions have more stringent rules and regulations than others, and this difference directly impacts the reputation and trustworthiness of the financial institutions operating within them. A bank operating in a jurisdiction with weak regulations may be more prone to issues, including fraud, hidden fees, or even the complete disappearance of the institution.

Reputable Offshore Banks and Financial Institutions

Identifying reputable offshore banks requires a proactive approach to research. Don’t rely solely on marketing materials. Look for institutions with a proven track record, a history of stability, and a commitment to customer service. A strong online presence, positive reviews from independent sources, and transparency in operations are significant indicators of a reliable offshore bank.

Researching and Verifying Offshore Providers

Scrutinizing the reputation of offshore providers involves multiple steps. Start by researching the bank’s history and financial standing. Look for information about its ownership structure, management team, and financial reports. Consider whether the institution has a long history and a proven track record of handling client accounts. Review any available regulatory filings or compliance information from the jurisdiction where the bank operates.

Finally, consult independent reviews and ratings from reputable financial institutions.

Evaluating the Credibility of Offshore Banking Institutions

Assessing the credibility of offshore banking institutions involves a multi-faceted approach. A well-established reputation is built on a solid foundation of transparency and regulatory compliance. Look for institutions that are licensed and regulated by their governing jurisdiction. The bank’s history, including any legal disputes or financial difficulties, should be thoroughly examined. Positive feedback from existing clients and a strong commitment to customer service are strong indicators of credibility.

Reputable Providers and Their Strengths and Weaknesses

| Offshore Bank/Institution | Strengths | Weaknesses |

|---|---|---|

| Example Bank A | Long history in the offshore market, strong regulatory compliance record, and a substantial client base. | Potentially higher fees compared to newer institutions, less emphasis on digital banking tools. |

| Example Bank B | Excellent customer service ratings, advanced digital banking platforms, and a modern approach to financial solutions. | Relatively newer in the offshore market, limited historical data for analysis. |

| Example Bank C | Known for its specialization in specific asset classes, providing tailored solutions for clients with unique financial needs. | Limited global reach, potential for niche-specific issues, potentially less diverse product offerings. |

Note: This table is for illustrative purposes only. The specific strengths and weaknesses of offshore banks will vary. Thorough research is essential to identify institutions that best suit your individual needs.

Common Pitfalls and Considerations

Source: financestrategists.com

Opening an offshore bank account can seem like a straightforward path to financial freedom, but it’s crucial to understand the potential pitfalls and risks. Navigating the complexities of international finance, regulations, and potential legal ramifications is essential for avoiding costly mistakes. This section will explore the common obstacles and considerations to help you make informed decisions.

Potential Risks and Liabilities

Offshore banking, while offering certain advantages, carries inherent risks. These risks extend beyond the initial setup and encompass ongoing compliance and potential legal issues. Misunderstandings of local regulations, non-compliance with reporting requirements, and even unwitting involvement in illicit activities can expose individuals to severe penalties and liabilities. These liabilities can range from substantial fines to criminal charges, impacting personal and financial well-being.

Finding the easiest offshore bank account often hinges on understanding the online process. Knowing how to open a foreign bank account online is key, as many offshore options streamline their application through digital channels. This often involves meticulous research and comparison of various providers, but the right platform can make the entire process significantly easier, making the best offshore bank account a more accessible goal.

how to open a foreign bank account online. Ultimately, the easiest offshore bank account often boils down to thorough online research and a clear understanding of the procedures involved.

Understanding these potential consequences is crucial before engaging in offshore banking.

Regulatory Changes and Their Impact

Financial regulations are dynamic and subject to frequent changes globally. These shifts can impact offshore accounts in various ways, potentially affecting account access, reporting requirements, or even the continued operation of the jurisdiction. Keeping abreast of these changes is vital to maintain compliance and avoid unforeseen consequences. For instance, the introduction of new tax reporting standards in a specific jurisdiction can suddenly require significant reporting obligations, and failure to comply can result in substantial penalties.

Proactive monitoring of regulatory updates is essential.

Importance of Professional Financial Advice

Navigating the complexities of offshore banking often requires expert guidance. Financial professionals specializing in international finance can provide valuable insights into the nuances of each jurisdiction, the implications of specific account types, and the potential tax and legal consequences. Seeking professional advice is not merely a suggestion; it’s a critical step in mitigating risks and ensuring compliance. A qualified financial advisor can provide tailored strategies for mitigating these risks, helping clients navigate the intricacies of offshore banking while minimizing potential liabilities.

An experienced advisor can help clients identify the right jurisdiction and account type based on their individual needs and circumstances.

Finding the easiest offshore bank account to open often hinges on understanding the nuances of overseas savings accounts. Overseas savings accounts can offer attractive features, but the key is to research thoroughly before committing. Ultimately, the easiest offshore bank account to open is the one that best aligns with your specific financial goals and regulations.

Potential Tax Implications

Tax implications of offshore accounts can vary significantly depending on the jurisdiction and the individual’s residency status. Understanding the tax implications is critical to avoid potential tax issues or audits. It’s crucial to consult with a tax professional to ensure that your offshore banking activities align with your tax obligations in your home jurisdiction. Tax evasion can result in significant penalties and legal repercussions.

Therefore, meticulous attention to tax implications and consulting with qualified tax advisors are essential steps.

Compliance and Reporting Requirements

Understanding and adhering to the compliance and reporting requirements of both the offshore jurisdiction and your home jurisdiction is paramount. Failure to comply with these requirements can lead to penalties and legal issues. The specifics of these requirements can vary greatly depending on the jurisdiction, and keeping track of these can be challenging. Professional guidance is highly recommended to avoid costly mistakes.

Strict adherence to reporting requirements and timely filings are crucial for maintaining the legality and legitimacy of offshore banking activities.

Illustrative Examples of Offshore Accounts

Offshore bank accounts, while offering potential benefits, often come with complexities and legal implications. Understanding how these accounts function in practice is crucial for evaluating their suitability. This section provides illustrative examples of offshore account structures and real-world applications. Consider these examples as hypothetical scenarios and not as recommendations for any specific course of action.Offshore account structures vary significantly, and the suitability of each depends on the individual’s financial situation, goals, and jurisdiction.

These examples showcase different strategies and their potential outcomes. They highlight the importance of thorough due diligence and professional advice before engaging with offshore banking.

Hypothetical Offshore Account Structures

Offshore accounts can be structured in diverse ways, tailored to different needs and risk tolerances. Here are a few examples:

- The Family Trust: A wealthy family establishes a trust in a low-tax jurisdiction to manage assets for future generations. This trust can hold various assets, including stocks, real estate, and even other offshore accounts. The trust structure provides asset protection and potentially minimizes tax liabilities for the beneficiaries. This approach offers potential estate planning benefits.

- The International Business Company (IBC): An entrepreneur operating a global business sets up an IBC in a tax-favorable jurisdiction. The IBC acts as a separate legal entity, offering liability protection and potentially reducing tax burdens associated with the business’s operations in multiple countries. The IBC can be used to hold assets and conduct international transactions.

- The Investment Portfolio: An individual looking to diversify their investment portfolio establishes accounts in different offshore jurisdictions to maximize returns and mitigate risk. Each account could hold specific investments, such as bonds, stocks, or cryptocurrency, based on market analysis and risk tolerance. The diversification strategy aims to balance potential gains with possible losses.

Case Studies of Offshore Account Usage

While anonymized, these case studies offer insights into how offshore accounts have been utilized:

| Case Study | Purpose | Jurisdiction | Benefits |

|---|---|---|---|

| Case 1 | Tax optimization | Cayman Islands | Reduced tax liabilities on international income, potentially higher investment returns. |

| Case 2 | Asset protection | British Virgin Islands | Shield assets from potential legal claims, particularly those arising from business ventures. |

| Case 3 | International investment | Switzerland | Access to a diversified international market, with potential for higher returns through specialized investments. |

These case studies illustrate various motivations for offshore account usage. It’s crucial to remember that these are simplified representations, and each situation is unique.

Offshore Account Benefits and Examples

Offshore accounts can offer potential advantages, but they also come with regulatory scrutiny and compliance obligations. Here are some examples:

- Tax Optimization: Certain jurisdictions offer favorable tax regimes, allowing individuals to potentially reduce their tax burden on international income or investment gains. This is dependent on individual circumstances and local regulations.

- Asset Protection: Offshore structures can potentially shield assets from lawsuits or creditors, although the effectiveness varies based on jurisdiction and legal context.

- Investment Diversification: Access to a wider range of investment opportunities in different jurisdictions, allowing for potential portfolio optimization and risk mitigation.

Final Conclusion

Opening an offshore bank account can be a powerful financial tool, but careful consideration is essential. This guide has equipped you with the knowledge to navigate the process, understand potential pitfalls, and choose a reputable provider. Remember, seeking professional financial advice is crucial to ensure your offshore banking strategy aligns with your specific financial goals and complies with all relevant regulations.

FAQ Section: Easiest Offshore Bank Account To Open

What are the common motivations for opening an offshore bank account?

Common motivations include tax optimization, asset protection, and enhanced financial privacy. Individuals may also seek to diversify their investment portfolio or manage wealth internationally.

What documents are typically required for opening an offshore bank account?

The specific documents vary by jurisdiction and account type. Generally, expect to provide proof of identity (passport, ID), proof of address, and potentially financial statements, depending on the bank’s requirements.

What are the potential risks associated with offshore accounts?

Potential risks include regulatory changes, potential tax implications in your home country, and reputational concerns if you choose a less-than-reputable provider. Thorough research and professional advice are critical to mitigate these risks.

How can I assess the reputation of an offshore banking institution?

Research the institution’s history, licensing, and regulatory compliance. Look for reviews and testimonials from other clients. Consider consulting with a financial advisor specializing in offshore accounts.

Leave a Reply